In 2026, Southeast Asia’s condo market is still defined by two simultaneous realities: deep, slow-moving oversupply in some large metro areas, and surprisingly resilient demand in specific segments and locations. The region is not in a single cycle. It is a patchwork of local affordability constraints, policy changes, migration patterns, and developer tactics that can keep headline prices stable even when clearing inventory takes years.

The clearest examples remain Metro Manila and Bangkok. Both built large pipelines during years when pre-selling was strong and credit was accommodative. Both then faced shocks—pandemic-era demand breaks, shifting investor appetite, and in Thailand’s case, a major quake in 2025 that changed how some buyers think about high-rise risk. The result is a market where transaction friction matters as much as “fundamentals”: downpayment terms, discounts, developer financing, and confidence in building quality.

Metro Manila: Oversupply is still there, but absorption is becoming more segmented

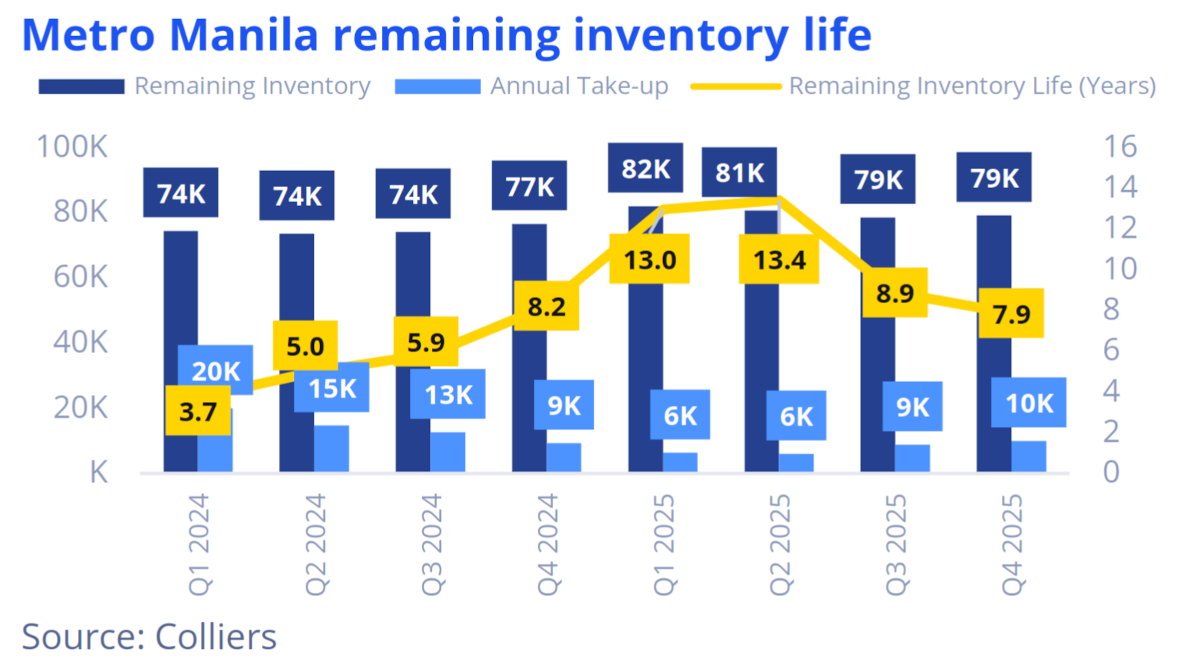

Metro Manila’s condo overhang will not disappear in 2026. The best available estimates still imply years of inventory to clear, even after some improvement from the worst point of the cycle. Colliers Philippines has said remaining inventory life improved to nearly eight years, down from a peak above 13 years.

What changed is where demand has returned. JLL Philippines’ year-end view of 2025 (a useful lead indicator for 2026 conditions) pointed to improved sales momentum in the midscale and upscale/luxury segments, with pre-selling take-up rising to 78.6% for midscale and 85.2% for upscale/luxury units, even as broader price indices softened. That is not a full-market recovery; it is a clearer split between projects that match today’s budgets and those that do not.

Gulf News, also drawing on Colliers commentary, described a sharp rebound in mid-income activity in specific submarkets. “Manila North” was cited as swinging from very low net take-up in early 2025 to over 1,000 units by Q3 2025. The same report noted that strategic pricing and flexible schemes were key drivers, and that ready-for-occupancy (RFO) inventories began tightening in some pockets. That is a demand story centered on affordability and terms, not a blanket return of speculative buying.

Clearing inventory: why “eight years” can still feel optimistic on the ground

Inventory-life numbers are useful, but they average across products that behave differently. A mid-income tower near transport or employment nodes can move quickly if it is priced for end-users and OFWs. A high-priced unit in a crowded luxury corridor can sit for years if buyers dislike the price, the developer’s reputation, or the area’s risk profile.

Even the Gulf News piece that described a mid-income rebound still framed Metro Manila as having about eight years’ worth of excess ready-for-occupancy (RFO) stock. Colliers’ own Q4 2025 reporting puts the context around that: unsold Metro Manila condo inventory at 79,200 units, with remaining inventory life improving to nearly 8 years from a 13.4-year peak in Q2 2025, alongside nearly 30,000 unsold RFO units concentrated in several submarkets. In practice, that helps explain why developers keep competing on payment structures and promos—they need steady sell-through, not just optimistic launch headlines.

This is where inventory clearance becomes financial, not purely “market-driven.” Because banks treat property as collateral, supervisors focus on ensuring lenders can absorb price declines. The BSP’s (The Philippine Central Bank) Financial Stability Report notes that it caps the value of real-estate collateral (60% of appraised value for secured/unsecured classification) to help ensure banks have enough buffer if property values fall. In the Philippines, where large property groups often sit within broader conglomerates with strong links to major lenders, there is added incentive to avoid disorderly repricing. That helps explain why developers lean on incentives and stretched payment terms to keep transactions moving, rather than resetting headline prices quickly.

Promos and payment engineering: Manila’s main clearing mechanism

Metro Manila developers have leaned heavily on price-and-terms engineering to move RFO and pre-selling units. Gulf News reported aggressive tactics: steep spot-cash discounts (reported up to 60%), lease-to-own options, and extended payment terms aimed at accelerating absorption of RFO inventory. These measures can shorten the sell-down period without forcing developers to publicly “cut list prices” across the board.

These schemes matter because the Philippines’ condo market still relies on the pre-selling model as a core funding structure. When end-user affordability is constrained, the industry’s “release valve” becomes longer downpayment schedules, smaller monthly amortizations during construction, and incentive bundles that reduce upfront friction.

Premier Possible’s Manila oversupply analysis has emphasized that the market can look healthier than it is if you focus only on launches and marketing. The practical signal is whether buyers can actually close and whether developers can keep RFO moving without turning to ever-more generous terms. The key question is not just demand; it is conversion to completed sales.

Price behavior in Manila: mid-market stability, luxury more sensitive to confidence shocks

Pricing in Metro Manila is not moving as a single series. In a Colliers Philippines briefing covered by InsiderPH, research director Joey Bondoc said the mid-income segment (₱2.5 million to ₱12 million) is driving the rebound and appears “isolated” from the political noise tied to the flood-control corruption scandal. He added that the controversy has weighed more on the luxury and ultra-luxury segment (roughly ₱15 million to ₱100 million per unit), where take-up has softened. That split fits a familiar pattern: mid-market demand is more necessity- and affordability-driven, while higher-end demand tends to be more sensitive to confidence shocks.

“You’re probably wondering, has the flood control issue affected the take-up? Well, we believe that the flood control mess has had some impact on the more expensive condo segments—luxury, ultra-luxury, P15 million, P100 million per unit,” Bondoc said.

At the same time, JLL pointed to continued OFW remittance support (citing 3.3% y/y growth in Q3 2025 cash remittances) and improved take-up in midscale and upscale/luxury pre-selling. Those signals can co-exist: prices can soften or stay flat while take-up improves, if absorption is being “bought” with incentives and if demand is concentrated in the best-located, best-priced projects.

Bangkok and Thailand: demand-soft market, selective recovery, and policy support that is timing-sensitive

Thailand’s 2026 condo story is more explicitly demand-soft in the aggregate, with some policy relief supporting transaction timing rather than changing the structural picture. Global Property Guide’s February 2026 update summarized Bank of Thailand data showing only 0.63% y/y growth in the nationwide residential price index in Q4 2025, and noted Bangkok and vicinities shifting into mild contraction (-0.70% y/y). It also described condos in Bangkok as broadly unchanged while single-detached houses declined.

Policy matters here. The same update highlighted reduced transfer and mortgage registration fees (down to 0.01% for eligible homes priced up to THB 7 million) and described these measures as supporting late-2025 momentum. Critically, the reduced-fee regime was described as running from April 2025 through June 30, 2026, which means part of the “rebound” is likely to be calendar-driven rather than a clean demand recovery.

This is a market where developers remain in intense price competition. Colliers’ Bangkok Snapshot Q2 2025 describes the condo sector as under pressure, with prices trending down. In its Bangkok Condominium Market Q4 2025 report, Colliers adds that developers are increasingly relying on competitive pricing, flexibility, and short-term sales incentives, with a clearer focus on clearing existing inventory. Together, that fits the broader picture in 2026: policy may help timing at the margin, but the underlying market is still being cleared through pricing discipline and targeted incentives rather than a broad, demand-led repricing.

The 2025 earthquake: why Bangkok’s high-rise conversation changed

Thailand’s condo market also carries a distinct 2025 shock. A major earthquake in Myanmar on March 28, 2025 was strongly felt in Bangkok, with reported building damage and fatalities, and it triggered immediate scrutiny of high-rise safety and inspection standards. Reuters and other outlets documented the event’s cross-border impact and the scale of disruption.

In 2026, the effect shows up less as a single price move and more as buyer selection behavior. Some demand shifts toward newer towers with strong engineering narratives, better building management, and clearer maintenance histories. In parallel, a portion of foreign residents and higher-income Thai households show stronger interest in low-rise alternatives—townhomes, detached houses, or villas in resort markets—because perceived structural risk is part of their decision set now, even if the statistical risk is hard to price. Premier Possible’s Bangkok oversupply-and-quake coverage treated this as a confidence and preference shock layered on top of an already crowded pipeline.

Bangkok’s high-end segment: a controlled recovery built on discipline and promotions

Bangkok’s strongest “green shoots” are in the luxury and prime rental segments, not in mass-market condos. A Real Estate Asia report (citing JLL) projected about 1,600 luxury units scheduled for completion in 2026, with average presale rates around 70.2%. It also described rents projected to rise 2.9% y/y by end-2026, capital values rebounding 3.1%, and yields stabilizing around 5.2%.

Those forecasts come with conditions. The same report said absorption was supported by promotional pricing strategies, with JLL attributing many transactions to projects offering steep discounts, and it noted that promotional campaigns for first-hand units continued to constrain resale price growth. Put simply: developers can keep the segment liquid, but at the cost of slower price appreciation.

An additional point worth noting is the strength of prime apartment occupancy in Bangkok’s central areas. The JLL-cited report described vacancy declining to 3.1% (the lowest in nearly three decades) amid a lack of new supply and steady demand from corporate occupiers and long-stay tenants. This aligns with a broader theme across the region: rental markets can tighten even while for-sale markets remain sluggish.

Foreign demand in Thailand: stable unit volumes, weaker value, and a tilt to smaller stock

Foreign demand has been a stabilizer in Thailand’s condo market, but the mix matters. The Nation, citing REIC data, reported 11,011 foreign condo transfers in January–September 2025 (essentially flat y/y), while total transfer value fell 14.2% to THB 44.1 billion. The article notes the “more units but less value” pattern as consistent with foreigners shifting toward more affordable condominiums rather than stepping up into larger-ticket purchases.

This is also where rules shape behavior. Premier Possible’s Thailand buying guide reiterates the practical core: foreigners can own freehold condo units within a building’s 49% foreign-ownership quota, and purchase funds generally must be remitted from overseas and evidenced via Thai banking documentation (FET) for registration. It also notes that many foreigners rent first, and that leasing remains a common, flexible pathway—especially when buyers are cautious about committing at the wrong point of the cycle.

Renting versus owning: why the “rental-first” approach is spreading

Across Bangkok—and in some Manila expat-heavy submarkets—renting is increasingly a deliberate choice rather than a fallback for those who “cannot buy.” In Bangkok’s high-end and luxury segment, JLL notes that many potential buyers favoured rental flexibility to reduce long-term financial obligations while the sales market remained cautious. This sits alongside a market where first-hand units are still being moved with steep promotions, which JLL says has constrained resale price appreciation. At the same time, JLL reports prime apartment demand in Bangkok’s CBD stayed firm, supported by corporate and long-stay tenants and limited new supply—another reason some households can choose to rent and wait, rather than lock in a purchase immediately.

In Manila, developers’ lease-to-own and extended-term offers blur the line between renting and buying. The market is effectively creating “trial periods” and lower-friction pathways to ownership as a way to keep absorption moving without headline price cuts.

This “rent-first” behavior also connects to global mobility. Southeast Asia remains attractive to mobile professionals and long-stay residents, but many of them prioritize flexibility. Where visa options and remote work allow long stays, the demand boost often shows up first in rentals and serviced residences, not in immediate condo purchases.

What is still being built: pipelines are narrowing, but not disappearing

Metro Manila

In Metro Manila, JLL’s 2025 year-end view pointed to a development pipeline through 2030, which also was cited by Context.ph, across major property types, including residential. That matters because “pipeline” is not just intent; it reflects land already secured, plans already filed, and financing models that typically depend on a steady cadence of launches. Even if developers slow new projects, completions from earlier cycles keep landing in the market.

At the top end, some of the most visible new stock is still concentrated in Makati and other established “core” addresses. The Estate Makati is positioned as a 60-storey, 188-unit tower on Ayala Avenue, with Foster + Partners listed as architect and SM Residences named as developer in project materials. A small unit count is not a guarantee of strong absorption, but it does signal how developers are trying to defend pricing: scarcity, privacy, and a narrower buyer pool that is less interest-rate sensitive than the mass market.

Another example is Laurean Residences in Legazpi Village, marketed as one tower with 70 floors and 388 units, with a target completion date of 2028. The takeaway is not that Makati is “immune” to the glut, but that developers still see depth at the high end—especially for larger unit sizes and projects designed around end-user preferences rather than small investor cuts. The trade-off is timing: when projects that deliver in 2028–2030 are sold today, the market is implicitly betting that current oversupply will be better absorbed by the time turnover arrives.

The biggest supply risk sits in multi-tower projects that add inventory in waves. The Observatory in Mandaluyong is a clear example. A Federal Land + Nomura Real Estate development described as eight condominium towers and 4,300 units on a 4.5-hectare site, with the first residential tower (“SORA Tower”) starting construction in June 2025. On the project’s own materials, the currently marketed residential component is listed at 706 total units, with a stated completion date of 31 December 2030. Developments like this can be rational—township-style phasing matches infrastructure build-out—but they also mean “new supply” remains a multi-year flow even if headline launches slow.

Bangkok

Bangkok shows a similar “narrowing, not stopping” pattern, but with a clearer split by segment. JLL reporting suggests around 1,600 luxury units are scheduled for completion in 2026, with developers concentrating launches in prime corridors and leaning into larger layouts and wellness-oriented amenities. That is still meaningful supply, but it is also far more disciplined than the pre-2020 surge in which luxury and near-luxury product multiplied across too many submarkets at once. The same reporting describes heavy reliance on promotions and discounts to move units, which is a sign that even “better” segments are not clearing without price incentives.

On-the-ground projects illustrate the segmentation. Still Sukhumvit 20 is marketed as a 30-storey project with 124 residential units (plus one commercial unit), a scale that fits the current luxury playbook: fewer units, bigger layouts, and a smaller buyer pool. Corporate disclosures also show institutional partners still backing this tier; Tokyo Tatemono says it joined SC Asset on the project and began VIP sales in November 2025. In other words, “luxury is controlled” does not mean “luxury is quiet”—it means supply is being rationed more carefully.

Outside the prime-luxury niche, Bangkok’s pipeline still includes large-volume towers where absorption risk is inherently higher. NUE Epic Asok–Rama 9 is presented as four high-rise towers with 3,107 units, planned for completion in July 2028 and located about 500 meters from MRT Phra Ram 9. Alongside these mega-projects are smaller, more defensive plays such as The Base Ratchada 19, a three-building, eight-storey project with 614 units on an approximately 8,000 sq.m. site. The combined picture is the point of this section: the pipeline is thinning and getting more selective, but it is not disappearing—so legacy oversupply has to be worked down while new stock continues to arrive.

Conglomerates, banks, and the “internal financing” advantage

A structural feature in several Southeast Asian markets is the role of conglomerates that have interests across development, construction, and banking. In the Philippines, large groups can influence affordability at the margin by bundling incentives and guiding credit access—especially when banks and property developers sit under the same corporate umbrella.

For example, Insider Philippines has described the SM group’s major financial and property components (including BDO Unibank and SM Prime) as part of a single conglomerate ecosystem. Ayala Land’s disclosures similarly reflect close-group relationships in financing channels within the Ayala group structure. This can help keep projects liquid, but it also ties housing cycles more tightly to banking exposure and credit conditions.

In 2026, the practical effect is visible in payment schemes. Developers can stretch downpayment timelines, offer “zero percent” teaser structures, or pre-arrange preferred-bank channels that make monthly payments look manageable—until the buyer faces the larger amortization step-up. In an oversupplied market, that ability to keep the funnel moving can delay price clearing, but it can also prevent a disorderly collapse.

Singapore: not an oversupply story, but a “product and policy” story

Singapore stands apart from Manila and Bangkok because supply is structurally constrained and policy is designed to discourage speculative churn. Instead of an inventory glut, the current debate is about unit sizes, affordability, and segmentation.

Recent reporting highlighted that new home sales surpassed 10,000 units for the first time in four years, a sign of improved activity. Separate coverage has also focused on the perception and reality that new homes are getting smaller, reinforcing that “headline demand” does not necessarily mean buyers are getting more space or better affordability outcomes.

Singapore’s luxury segment has also been active, but it is heavily policy-shaped. The key regional takeaway is that Singapore’s market stress is less about excess towers and more about the controlled scarcity model—and the distributional effects that come with it.

Malaysia: Kuala Lumpur’s high-rise overhang versus Johor’s momentum

Malaysia’s condo picture is also uneven, with Kuala Lumpur showing lingering high-rise overhang characteristics while other areas, especially Johor, benefit from infrastructure and cross-border dynamics. The Edge reported mixed residential conditions: prime KL neighborhoods saw rental growth around 5%–10%, while the sub-sale market slowed as buyers became cautious. It also reported that oversupply continued to weigh on high-rise developments in dense urban corridors, and that much of the overhang was legacy stock rather than new supply, with a large share of unsold units remaining on the market for six to ten years.

Policy and taxes are part of the 2026 picture. The Edge noted higher foreign-buyer stamp duty taking effect in January 2026, which can affect demand at higher price points. Meanwhile, Johor Bahru was described as a bright spot supported by the RTS Link and special economic zone momentum.

Kuala Lumpur’s premium counterpoint: Merdeka Residences and “destination” towers

If you look only at glut headlines, you miss the premium segment’s strategy: large integrated projects that sell a location, a skyline address, and services—often closer to the “branded residence” playbook than the classic condo tower model. Premier Possible’s coverage of Merdeka Residences positions it as part of Kuala Lumpur’s ultra-prime ecosystem tied to the Merdeka 118 precinct, aimed at buyers who are less sensitive to broader high-rise oversupply and more focused on asset quality and place-making. This is where pricing power tends to survive longest.

Indonesia (Jakarta): bifurcation, liquidity caution, and the credit channel

Jakarta does not fit the same “condo oversupply” story as Manila or Bangkok. The more visible pattern is demand caution in the apartment market, even as other real estate segments keep moving. A Savills-linked market update carried by Real Estate Asia said apartment demand remained constrained in Q3 2025, and that the government’s VAT incentive had not yet lifted sales because buyers were prioritising liquidity and cash preservation.

That demand restraint sits alongside an active financing system that still matters for housing outcomes. In February 2026, IDNFinancials reported that at state-owned lender Bank Tabungan Negara (BTN), housing loans dominated the portfolio (82% of total lending in 2025) and the mortgage segment grew 8.7% to IDR 304.2 trillion. It also noted housing construction loans fell sharply (down 12.1%), a useful clue that credit can support end-buyer demand even while new-building finance turns more selective.

For condo-style projects, the practical result is a “sorting” market. When buyers focus on cash buffers, best-located and best-executed stock has a better chance of clearing than generic inventory, and incentives may be less effective than in a credit-driven upswing. The same Real Estate Asia update framed the apartment slowdown as part of a broader caution cycle, not as a single-sector problem.

What to watch next is whether mortgage growth translates into sustained absorption for urban apartments, or mostly supports landed and affordable formats. If liquidity preference stays high, Jakarta’s condo market is likely to keep bifurcating by location, pricing tier, and perceived build quality—with “prime” holding up better than the middle—rather than moving in a clean, citywide recovery.

Branded residences: a regional strategy to escape the commodity condo trap

One of the clearest region-wide responses to oversupply is differentiation: branded residences, serviced-living components, and amenity-heavy positioning. Branded residences are defined as homes developed with a luxury brand affiliation—often hospitality—and sold with a service promise, not just a unit.

A key reason they attract buyers is simple economics: branded projects often command a meaningful price premium versus comparable non-branded stock, reflecting what buyers are paying for—brand trust, fit-and-finish expectations, and the “known quantity” of a globally managed product. Premier Possible cites Savills’ 2024–2025 findings that branded residences average about a 30% premium, and that the premium can be higher in certain markets.

They also reduce operational uncertainty for remote owners. Many buyers in this tier want hands-off ownership: predictable building management, concierge-style services, and clearer standards around maintenance and resident experience. That preference is one reason hotel brands still dominate the category; Savills’ own summary notes luxury hospitality brands represent a large majority of global branded residences.

The rental angle matters too. Branded residences are often designed to support rental program optionality—either through hotel-managed rental pools or through a product spec that is easier to lease at higher rates (furnishing, services, front desk, housekeeping options, and building-level amenities). That dovetails with the growth of high-income long-stay travelers who expect reliable “hotel-plus” living—strong internet, concierge support, wellness spaces, and turnkey setups—rather than informal landlord arrangements.

For developers, branded residences can also be a financing and de-risking tool. Hospitality Design quotes industry voices describing the segment as relatively resilient because it targets high-net-worth buyers and can help sales velocity and underwriting in mixed-use projects (including hotels), which matters when conventional condo sell-through is slow. The same coverage points to the scale of the sector, with hundreds of projects completed and hundreds more in the pipeline by 2030

This does not solve the mass-market backlog. But it can protect a slice of the pipeline and concentrate demand in a smaller set of projects while older commodity towers keep competing on price, incentives, and payment terms.

What to watch through 2026: the signals that matter more than launch headlines

In oversupplied condo markets, the headline question is not “who is launching.” It is who is clearing. Announcements and marketing can stay busy even when the backlog is large. The cleaner read comes from outcomes: completed sales, occupancy, and whether inventory life is actually trending down.

In Metro Manila, watch whether the mid-income rebound converts into sustained closings without ever-richer terms. RFO absorption and sell-through matter more than reservations. If inventory life keeps falling while promos stabilize, the market is normalizing. If the “improvement” comes mainly from delayed completions or longer payment ladders, clearance is still slow.

In Bangkok, the market can show firm rentals alongside soft sales. The key signal is whether promotions keep substituting for price growth, and whether the rent-first approach remains common among higher-end households. Policy timing also matters: the real test is what happens after June 30, 2026, when reduced transfer and mortgage registration fees expire.

In Singapore, the story is less about overhang and more about product and policy constraints: whether demand holds as supply stays managed, and whether unit sizing and affordability pressures continue to shape what buyers will accept. In Kuala Lumpur, watch the split between high-rise legacy stock and “destination” projects; the clearing question is whether older inventory keeps being absorbed without deeper repricing, while premium nodes defend pricing power. In Jakarta, the key is whether mortgage growth translates into sustained apartment absorption, or mainly supports other housing formats; the likely outcome is continued bifurcation by location and quality.

Across the region, the market is re-sorting by affordability, build quality, and trust in management. Premium projects can stay liquid while commodity towers compete on terms. The practical 2026 takeaway is that Manila and parts of Bangkok still face multi-year clearance, while Singapore, Kuala Lumpur, and Jakarta are more about segmentation than a single cycle. Progress will be visible in fewer incentives, faster closings, and healthier resale pricing across more submarkets—not just a handful of exceptional projects.